Research News and Market Data on FAT

LOS ANGELES, Oct. 30, 2024 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”) today reported financial results for the fiscal third quarter ended September 29, 2024.

Andy Wiederhorn, Chairman of FAT Brands, said, “Over the last three years, we have expanded our brand portfolio to include 18 distinct concepts while our footprint has increased tenfold, now encompassing over 2,300 locations across more than 40 countries and 49 U.S. states or territories. We opened 22 new units during the third quarter, bringing our year-to-date openings to 71 new units and are on track to end the year with 100 new units.”

Wiederhorn added, “We have signed 225 development deals year-to-date versus 226 deals in all of 2023, bringing our current development pipeline to approximately 1,000 locations. This is a strong indicator of confidence within the FAT franchise system.”

Ken Kuick, Co-Chief Executive Officer of FAT Brands, said, “We continue to prioritize accelerated growth in our Polished Casual category, particularly through Twin Peaks, our fastest-growing concept. Year to date, we opened nine new lodges, bringing our total to 115 locations. We also completed our first Smokey Bones to Twin Peaks conversion in Lakeland, Florida during the third quarter, with our second conversion underway and several more planned for next year.”

Rob Rosen, Co-Chief Executive Officer of FAT Brands, said, “In May, Twin Peaks and Smokey Bones, as a combined entity, took a significant step towards becoming a standalone public company. We view this potential IPO or alternative transaction as a strategic opportunity to unlock value for FAT shareholders. Shortly, we intend to refinance Twin Peaks’ securitization debt, which will optimize our financial structure prior to any IPO or other transaction.”

Fiscal Third Quarter 2024 Highlights

- Total revenue grew 31.1% to $143.4 million compared to $109.4 million in the fiscal third quarter of 2023

- System-wide sales grew 6.4% in the fiscal third quarter of 2024 compared to the prior year fiscal quarter

- Year-to-date system-wide same-store sales declined 2.7% compared to the prior year

- 22 new store openings during the fiscal third quarter of 2024

- Net loss of $44.8 million, or $2.74 per diluted share, compared to $24.7 million, or $1.59 per diluted share, in the fiscal third quarter of 2023

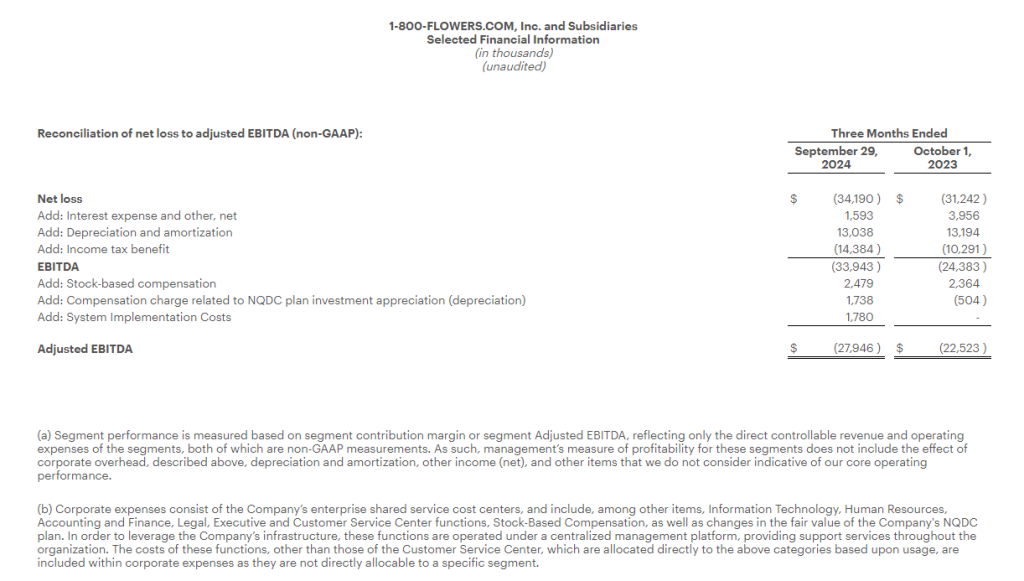

- EBITDA(1) of $1.7 million compared to $10.8 million in the fiscal third quarter of 2023

- Adjusted EBITDA(1) of $14.1 million compared to $21.9 million in the fiscal third quarter of 2023

- Adjusted net loss(1) of $38.0 million, or $2.34 per diluted share, compared to adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, in the fiscal third quarter of 2023

(1) EBITDA, adjusted EBITDA and adjusted net loss are non-GAAP measures defined below, under “Non-GAAP Measures”. Reconciliation of GAAP net loss to EBITDA, adjusted EBITDA and adjusted net loss are included in the accompanying financial tables.

Summary of Fiscal Third Quarter 2024 Financial Results

Total revenue increased $34.0 million, or 31.1%, in the third quarter of 2024 to $143.4 million compared to $109.4 million in the same period of 2023, driven by the acquisition of Smokey Bones in September 2023 and revenues from new restaurant openings.

Costs and expenses consist of general and administrative expense, cost of restaurant and factory revenues, depreciation and amortization, refranchising net loss and advertising fees. Costs and expenses increased $49.5 million, or 48.1%, in the third quarter of 2024 to $152.2 million compared to the same period in the prior year, primarily due to the acquisition of Smokey Bones in September 2023 and increased activity from Company-owned restaurants and the Company’s factory.

General and administrative expense increased $10.0 million, or 41.0%, in the third quarter of 2024 to $34.5 million compared to $24.5 million in the same period in the prior year, primarily due to the acquisition of Smokey Bones in September 2023 and increased professional fees related to pending litigation.

Cost of restaurant and factory revenues was related to the operations of the company-owned restaurant locations and dough factory and increased $37.6 million, or 63.6%, in the third quarter of 2024, primarily due to the acquisition of Smokey Bones in September 2023 and higher company-owned restaurant sales.

Depreciation and amortization increased $3.7 million, or 52.5% in the third quarter of 2024 compared to the same period in the prior year, primarily due to the acquisition of Smokey Bones in September 2023 and depreciation of new property and equipment at company-owned restaurant locations.

Refranchising net loss, comprised of restaurant operating costs, net of food sales, was $0.2 million in the third quarter of 2024 compared to $0.4 million in the third quarter of 2023.

Advertising expenses decreased $1.6 million in the third quarter of 2024 compared to the prior year period. These expenses vary in relation to advertising revenues.

Total other expense, net, for the third quarter of 2024 and 2023 was $35.8 million and $32.6 million, respectively, which is inclusive of interest expense of $35.5 million and $29.7 million, respectively. This increase is primarily due to new debt issuances. Total other expense, net, for the third quarter of 2023 also consisted of a $2.7 million net loss on the extinguishment of debt.

Adjusted net loss(1) was $38.0 million, or $2.34 per diluted share, compared to adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, in the fiscal third quarter of 2023.

Key Financial Definitions

New store openings – The number of new store openings reflects the number of stores opened during a particular reporting period. The total number of new stores per reporting period and the timing of stores openings has, and will continue to have, an impact on our results.

Same-store sales growth – Same-store sales growth reflects the change in year-over-year sales for the comparable store base, which we define as the number of stores open and in the FAT Brands system for at least one full fiscal year. For stores that were temporarily closed, sales in the current and prior period are adjusted accordingly. Given our focused marketing efforts and public excitement surrounding each opening, new stores often experience an initial start-up period with considerably higher than average sales volumes, which subsequently decrease to stabilized levels after three to six months. Additionally, when we acquire a brand, it may take several months to integrate fully each location of said brand into the FAT Brands platform. Thus, we do not include stores in the comparable base until they have been open and in the FAT Brands system for at least one full fiscal year.

System-wide sales growth – System-wide sales growth reflects the percentage change in sales in any given fiscal period compared to the prior fiscal period for all stores in that brand only when the brand is owned by FAT Brands. Because of acquisitions, new store openings and store closures, the stores open throughout both fiscal periods being compared may be different from period to period.

Conference Call and Webcast

FAT Brands will host a conference call and webcast to discuss its fiscal third quarter 2024 financial results today at 5:00 PM ET. Hosting the conference call and webcast will be Andy Wiederhorn, Chairman of the Board, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call can be accessed live over the phone by dialing 1-877-704-4453 from the U.S. or 1-201-389-0920 internationally. A replay will be available after the call until Wednesday, November 20, 2024, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 13748855. The webcast will be available at www.fatbrands.com under the “Investors” section and will be archived on the site shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Smokey Bones, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses and franchises and owns approximately 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the future financial and operating results of the Company, the timing and performance of new store openings, our ability to conduct future accretive acquisitions and our pipeline of new store locations. Forward-looking statements generally use words such as “expect,” “foresee,” “anticipate,” “believe,” “project,” “should,” “estimate,” “will,” “plans,” “forecast,” and similar expressions, and reflect our expectations concerning the future. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other risks and uncertainties that could cause our actual results to differ materially from our current expectations and from the forward-looking statements contained in this press release. We undertake no obligation to update any forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Non-GAAP Measures (Unaudited)

This press release includes the non-GAAP financial measures of EBITDA, adjusted EBITDA and adjusted net loss.

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. We use the term EBITDA, as opposed to income from operations, as it is widely used by analysts, investors, and other interested parties to evaluate companies in our industry. We believe that EBITDA is an appropriate measure of operating performance because it eliminates the impact of expenses that do not relate to business performance. EBITDA is not a measure of our financial performance or liquidity that is determined in accordance with generally accepted accounting principles (“GAAP”), and should not be considered as an alternative to net loss as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP.

Adjusted EBITDA is defined as EBITDA (as defined above), excluding expenses related to acquisitions, refranchising loss, impairment charges, and certain non-recurring or non-cash items that the Company does not believe directly reflect its core operations and may not be indicative of the Company’s recurring business operations.

Adjusted net loss is a supplemental measure of financial performance that is not required by or presented in accordance with GAAP. Adjusted net loss is defined as net loss plus the impact of adjustments and the tax effects of such adjustments. Adjusted net loss is presented because we believe it helps convey supplemental information to investors regarding our performance, excluding the impact of special items that affect the comparability of results in past quarters to expected results in future quarters. Adjusted net loss as presented may not be comparable to other similarly titled measures of other companies, and our presentation of adjusted net loss should not be construed as an inference that our future results will be unaffected by excluded or unusual items. Our management uses this non-GAAP financial measure to analyze changes in our underlying business from quarter to quarter based on comparable financial results.

Reconciliations of net loss presented in accordance with GAAP to EBITDA, adjusted EBITDA and adjusted net loss are set forth in the tables below.

Investor Relations:

ICR

Michelle Michalski

ir-fatbrands@icrinc.com

646-277-1224

Media Relations:

Erin Mandzik

emandzik@fatbrands.com

860-212-6509

FAT Brands Inc. Consolidated Statements of Operations

Click Here for Full Report