Research News and Market Data on SMT

MARCH 28, 2023

DownloadPDF Format (opens in new window)

Conference Call and Webcast will be held on March 29, 2023 at 11:00am ET

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (“Sierra Metals” or the “Company”) announces fourth quarter and year-end 2022 consolidated financial results. All amounts are in US dollars, unless otherwise noted.

Fourth Quarter and Year-End 2022 Operating and Financial Highlights

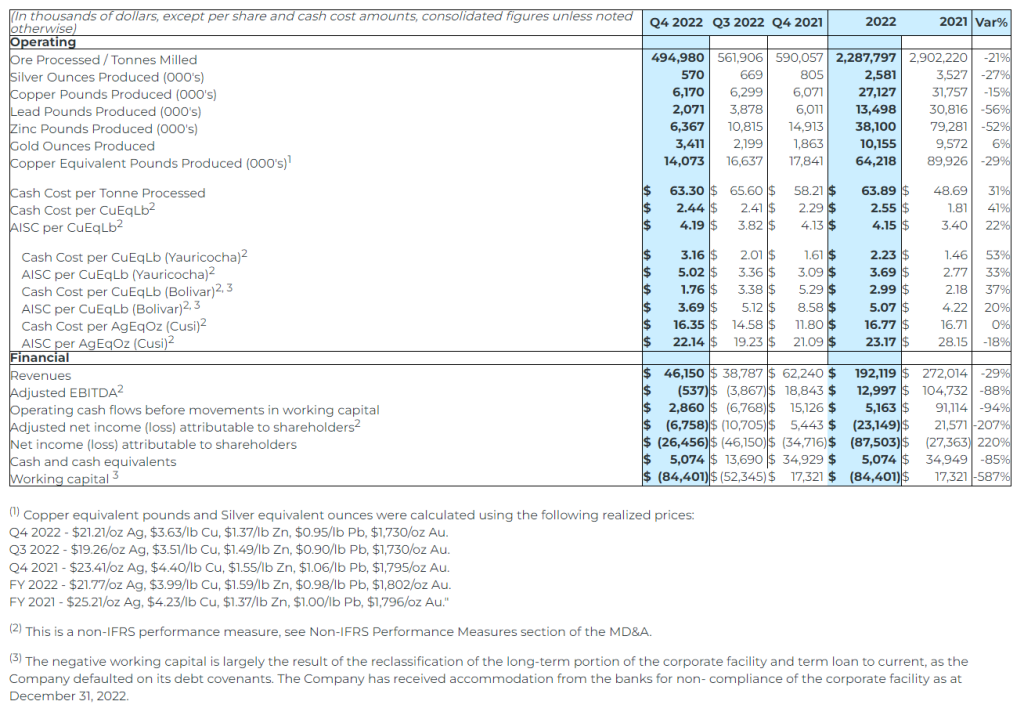

- Revenue from metals payable of $46.2 million in Q4 2022 and $192.1 million in 2022.

- Adjusted EBITDA(1) of ($0.5) million in Q4 2022 and $13.0 million in 2022.

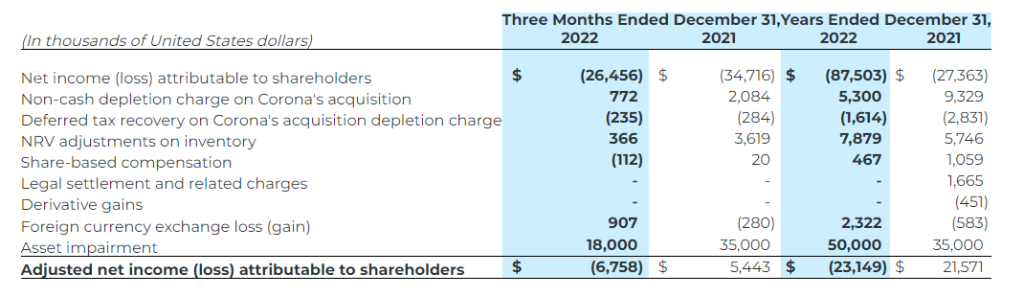

- Net loss attributable to shareholders for Q4 2022 of $26.5 million, or $0.16 per share and $87.5 million, or $0.53 per share in 2022.

- Net loss of $88.3 million, or $0.54 in 2022, which includes impairment charges of $25.0 million for the Bolivar mine and $25.0 million for the Cusi mine; and $5.3 million non-cash depletion.

- Cash and cash equivalents as at December 31, 2022 was $5.1 million; negative working capital of $84.4 million.

- The focus in 2023 is to improve safety practices, reduce costs, improve productivity through increased equipment availability.

On March 13, 2023, the Company improved short-term liquidity through refinancing $6,250,000 of debt repayments due March 2023, with negotiations ongoing to refinance a total of $18,750,000 of term loan amortization payments due in 2023.

Ernesto Balarezo Valdez, Sierra Metals’ Interim CEO comments, “Sierra Metals enters 2023 with positive momentum. Since the start of 2023, we have stabilized our operations and begun to implement a program to optimize our operating performance, all with safety as the top priority. The expected operational improvements, alongside the corporate initiatives to improve our balance sheet, which includes the recently announced debt refinancing initiatives, has set the stage for Sierra Metals to increase production, lower costs and improve our financial position.”

(1) This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Strategic Update

As first announced on October 18, 2022, a special committee comprised of the Company’s independent directors (the “Special Committee”) is undertaking a strategic review process. The mandate of the Special Committee includes exploring, reviewing and considering options to optimize the operations of the Company and possible financing, restructuring and strategic options in the best interests of the Company. The Company has engaged CIBC Capital Markets as a financial advisor in this process.

The Special Committee continues to evaluate certain strategic alternatives. The Company will report to shareholders upon completion of the Special Committee’s review. Concurrently, over the course of the strategic review process the Special Committee and the management team have identified and have implemented a number of opportunities to improve the Company’s operational and financial position.

Progress made to-date includes the following:

- Successfully implementing a transition of executive level management.

- Organizational changes designed to create a shift in the corporate culture and instill a more “hands-on” approach to operations.

- Placing a renewed emphasis on safety and employee engagement. The Company has hired a VP of Health and Safety, instituted new safety protocols across all of its operations, increased training and communication efforts, and invested in remote-controlled equipment which is designed to reduce risk of injury.

- Streamlining operations to reduce costs, and refinancing debt obligations in order to preserve working capital as production levels improve.

- Advancing discussions with secured lenders on refinancing of material short-term obligations, and steps to improve short-term liquidity through ancillary financing arrangements.

- Initiatives to increase productivity at the mines, including increasing asset utilization, focused underground development of mine sequencing, and improvements to ventilation and pumping systems.

- Prioritizing spending to focus resources on the Company’s core assets at Yauricocha and Bolivar.

- Initiating activities designed to identify additional mineral resources at the Yauricocha and Bolivar mines to sustain long-term production increases.

- Enhancements to internal financial forecasting, reporting and integration of information across functions to ensure timely decision making.

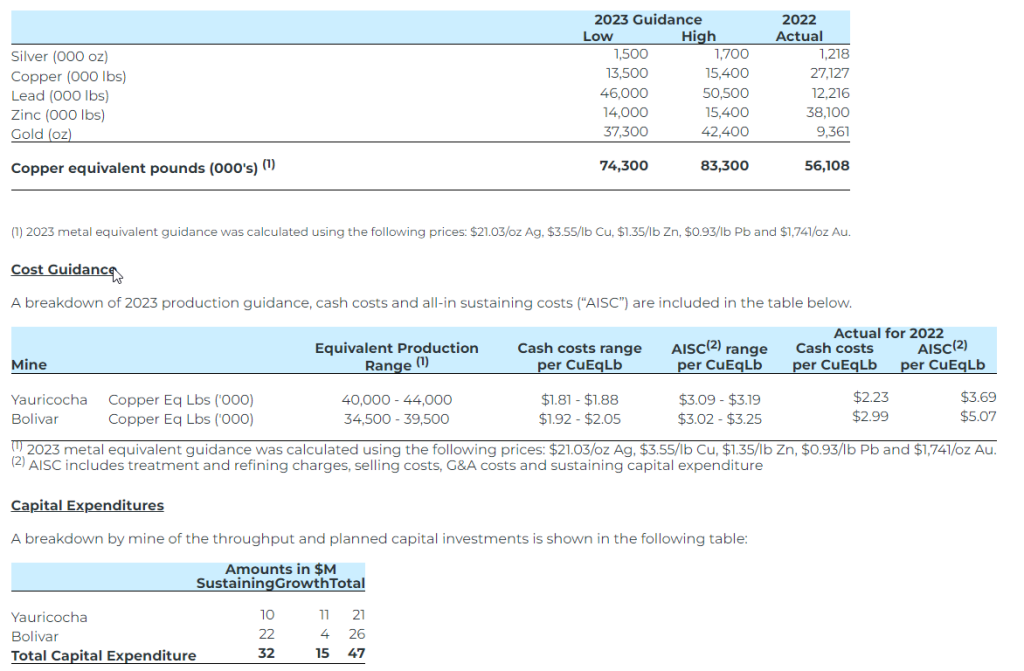

2023 Guidance

Production Guidance

The Bolivar mine exited fourth quarter 2022 with improved operations and expectations of continued improved performance throughout 2023. The Yauricocha mine is expected to gradually and safely ramp up production throughout 2023 at the current depth. Meanwhile, Yauricocha’s focus will remain on obtaining the necessary permits to access the deeper, high-grade ore bodies.

The table summarizing 2023 production guidance from the Yauricocha and the Bolivar mines is provided below. Management considers the Cusi mine as ‘non-core’ and it has been excluded from the guidance.

Total sustaining capital for 2023, excluding Cusi, is expected to be $32.0 million, mainly comprised of mine development ($3.0 million) and drainage ($2.3 million) in Yauricocha, and mine development ($11.3 million), infill drilling ($5.3 million) and equipment replacement ($3.9 million) at the Bolivar mine.

Growth capital for 2023, projected at $15.0 million, includes costs of tailings dam expansion ($5.6 million) and Yauricocha shaft ($3.2 million) in Peru. Growth capital at Bolivar includes costs of the tailings dam and the starter dam.

Management will continue to review performance throughout the year, while exploring value enhancing opportunities.

Conference Call & Webcast

The Company will host a conference call on Wednesday, March 29, 2023, at 11:00 AM EDT to discuss the results. Details of the conference call and webcast are as follows:

| Date: | March 29, 2023 | |

| Time: | 11:00 am ET | |

| Webcast: | https://events.q4inc.com/attendee/111210337 | |

| Telephone: | Access code: 077974 | |

| Canada: 1 833 950 0062 (toll free) | ||

| USA: 1 844 200 6205 (toll free) | ||

| Other: 1 929 526 1599 |

The webcast, presentation slides and 2022 Financial Statements and Management Discussion and Analysis will be available at www.sierrametals.com, with an archive of the webcast available for 180 days.

Summary of Operating and Financial Results

The information provided below are excerpts from the Company’s Annual Financial Statements and Management’s Discussion and Analysis, which are available on the Company’s website (www.sierrametals.com) and on SEDAR (www.sedar.com) under the Company’s profile.

2022 Consolidated Financial Summary

- Revenue from metals payable of $192.1 million in 2022, a decrease of 29% from 2021 annual revenue of $272.0 million. Lower revenue resulted from the decrease in throughput and grades at the Yauricocha and Bolivar mines;

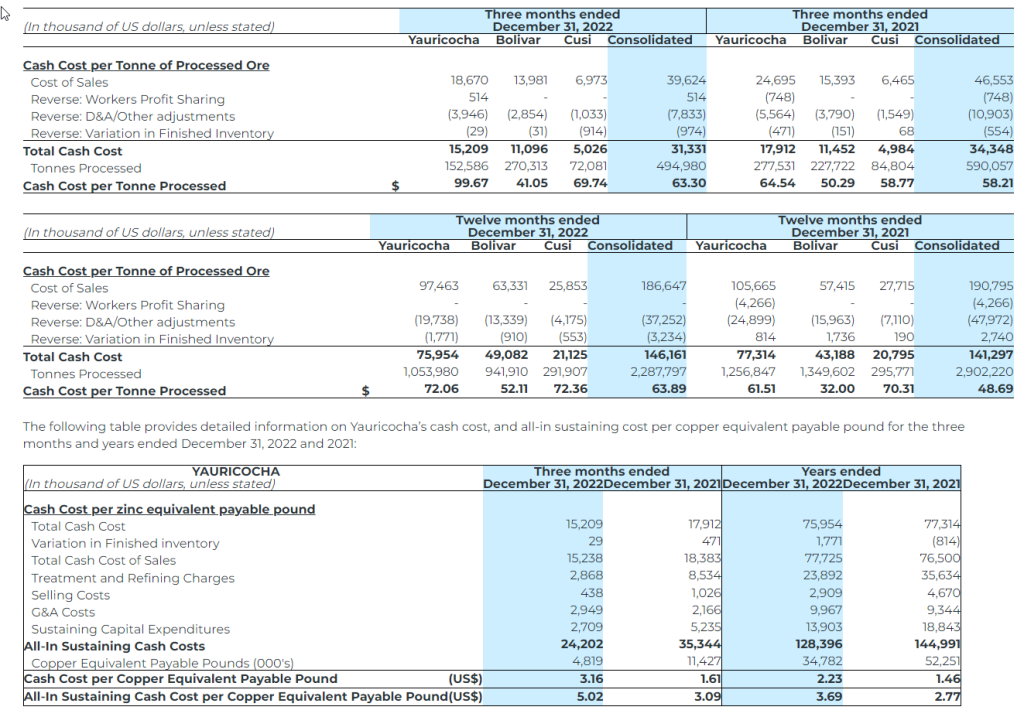

- Yauricocha’s cash cost per copper equivalent payable pound(1) was $2.23 (2021 – $1.46), and AISC per copper equivalent payable pound(1) of $3.69 (2021 – $2.77);

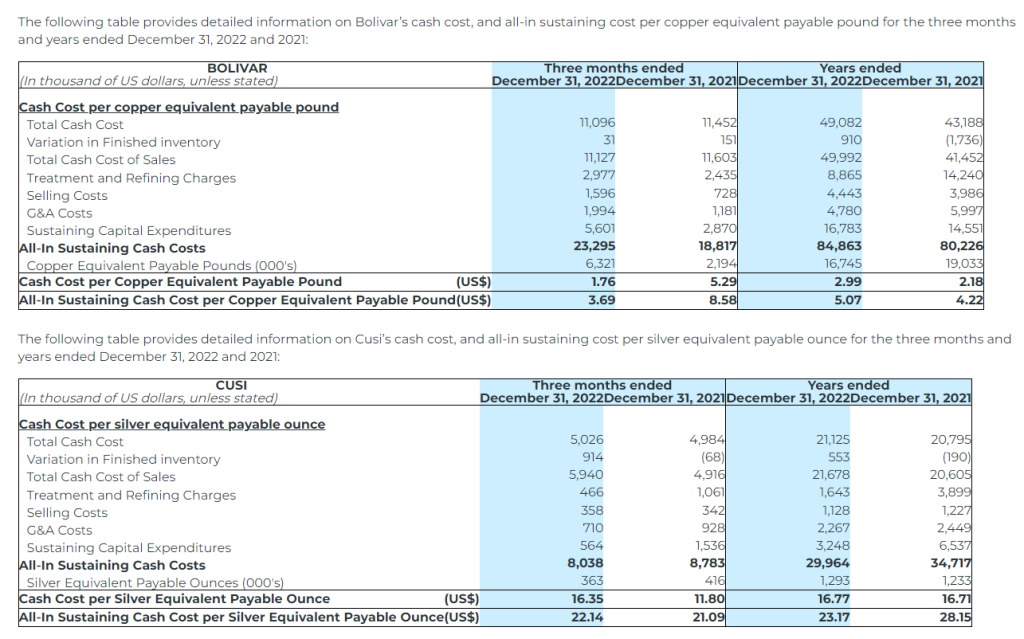

- Bolivar’s cash cost per copper equivalent payable pound(1) was $2.99 (2021 – $2.18), and AISC per copper equivalent payable pound(1) was $5.07 (2021 – $4.22);

- Cusi’s cash cost per silver equivalent payable ounce(1) was $16.77 (2021 – $16.71), and AISC per silver equivalent payable ounce(1) was $23.17 (2021 – $28.15);

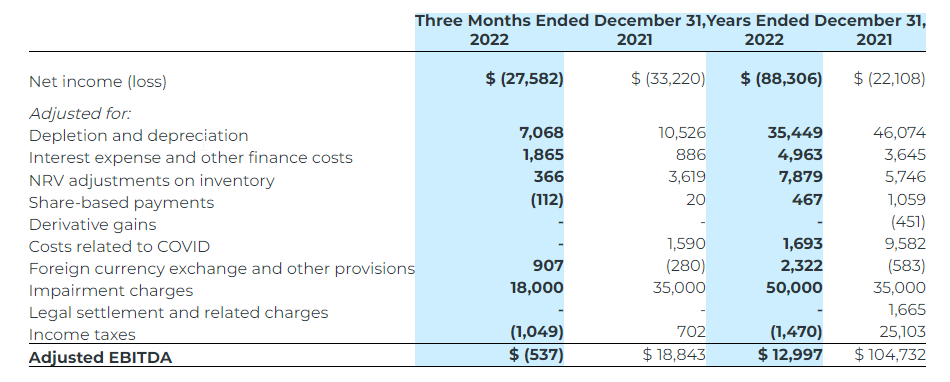

- Adjusted EBITDA(1) of $13.0 million for 2022, a decrease from the adjusted EBITDA(1) of $104.7 million for 2021;

- Net loss attributable to shareholders for 2022 was $87.5 million or $0.53 per share (2021: net loss of $27.4 million, $0.17 per share). Net loss for the year ended 2022 includes an impairment charge of $25.0 million on the Bolivar mine and $25.0 million on the Cusi mine (2021: impairment of $35.0 million on the Cusi mine);

- Adjusted net loss attributable to shareholders(1) of $23.1 million, or $0.14 per share, for 2022 compared to the adjusted net income(1) of $21.6 million, or $0.13 per share for 2021;

- A large component of the net income (loss) for every period is the non-cash depletion charge in Peru, which was $5.3 million for 2022 (2021: $9.3 million). The non-cash depletion charge is based on the aggregate fair value of the Yauricocha mineral property at the date of acquisition of Sociedad Minera Corona S.A. de C.V. (“Corona”) of $371.0 million amortized over the life of the mine;

- Cash flow generated from operations before movements in working capital of $5.2 million for 2022 was lower than the $91.1 million in 2021, mainly due to lower revenues and higher operating costs; and

- Cash and cash equivalents of $5.1 million and working capital of $(84.4) million as at December 31, 2022 compared to $34.9 million and $17.3 million, respectively, at the end of 2021. Cash and cash equivalents decreased during 2022 as the $38.3 million used in investing activities exceeded the $1.1 million generated from financing activities and $7.3 million generated from operating activities.

(1) This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Non-IFRS Performance Measures

The non-IFRS performance measures presented do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be directly comparable to similar measures presented by other issuers.

Non-IFRS reconciliation of adjusted EBITDA

EBITDA is a non-IFRS measure that represents an indication of the Company’s continuing capacity to generate earnings from operations before taking into account management’s financing decisions and costs of consuming capital assets, which vary according to their vintage, technological currency, and management’s estimate of their useful life. EBITDA comprises revenue less operating expenses before interest expense (income), property, plant and equipment amortization and depletion, and income taxes. Adjusted EBITDA has been included in this document. Under IFRS, entities must reflect in compensation expense the cost of share-based payments. In the Company’s circumstances, share-based payments involve a significant accrual of amounts that will not be settled in cash but are settled by the issuance of shares in exchange for cash. As such, the Company has made an entity specific adjustment to EBITDA for these expenses. The Company has also made an entity-specific adjustment to the foreign currency exchange (gain)/loss. The Company considers cash flow before movements in working capital to be the IFRS performance measure that is most closely comparable to adjusted EBITDA.

The following table provides a reconciliation of adjusted EBITDA to the consolidated financial statements for the three months and years ended December 31, 2022 and 2021:

Non-IFRS Reconciliation of Adjusted Net Income (Loss)

Adjusted net income (loss) attributable to shareholders represents net income (loss) attributable to shareholders excluding certain impacts, net of taxes, such as non-cash depletion charge due to the acquisition of Corona, impairment charges and reversal of impairment charges, write-down of assets, and certain non-cash and non-recurring items including but not limited to share-based compensation and foreign exchange (gain) loss.The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors may want to use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance in accordance with IFRS.

The following table provides a reconciliation of adjusted net income (loss) to the consolidated financial statements for the three months and years ended December 31, 2022 and 2021:

Cash Cost per Silver Equivalent Payable Ounce and Copper Equivalent Payable Pound

The Company uses the non-IFRS measure of cash cost per silver equivalent ounce and copper equivalent payable pound to manage and evaluate operating performance. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance and ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The Company considers cost of sales per silver equivalent payable ounce and copper equivalent payable pound to be the most comparable IFRS measure to cash cost per silver equivalent payable ounce, copper equivalent payable pound, and zinc equivalent payable pound, and has included calculations of this metric in the reconciliations within the applicable tables to follow.

All-in Sustaining Cost per Silver Equivalent Payable Ounce and Copper Equivalent Payable Pound

All‐In Sustaining Cost (“AISC”) is a non‐IFRS measure and was calculated based on guidance provided by the World Gold Council (“WGC”) in June 2013. WGC is not a regulatory industry organization and does not have the authority to develop accounting standards for disclosure requirements. Other mining companies may calculate AISC differently as a result of differences in underlying accounting principles and policies applied, as well as differences in definitions of sustaining versus development capital expenditures.

AISC is a more comprehensive measure than cash cost per ounce/pound for the Company’s consolidated operating performance by providing greater visibility, comparability and representation of the total costs associated with producing silver and copper from its current operations.

The Company defines sustaining capital expenditures as, “costs incurred to sustain and maintain existing assets at current productive capacity and constant planned levels of productive output without resulting in an increase in the life of assets, future earnings, or improvements in recovery or grade. Sustaining capital includes costs required to improve/enhance assets to minimum standards for reliability, environmental or safety requirements. Sustaining capital expenditures excludes all expenditures at the Company’s new projects and certain expenditures at current operations which are deemed expansionary in nature.”

Consolidated AISC includes total production cash costs incurred at the Company’s mining operations, including treatment and refining charges and selling costs, which forms the basis of the Company’s total cash costs. Additionally, the Company includes sustaining capital expenditures and corporate general and administrative expenses. AISC by mine does not include certain corporate and non‐cash items such as general and administrative expense and share-based payments. The Company believes that this measure represents the total sustainable costs of producing silver and copper from current operations and provides the Company and other stakeholders of the Company with additional information of the Company’s operational performance and ability to generate cash flows. As the measure seeks to reflect the full cost of silver and copper production from current operations, new project capital and expansionary capital at current operations are not included. Certain other cash expenditures, including tax payments, dividends and financing costs are also not included.

The following table provides a reconciliation of cash costs to cost of sales, as reported in the Company’s consolidated statement of income for the three months and years ended December 31, 2022 and 2021:

Additional Non-IFRS Measures

The Company uses other financial measures, the presentation of which is not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. The following other financial measures are used:

- Operating cash flows before movements in working capital – excludes the movement from period-to-period in working capital items including trade and other receivables, prepaid expenses, deposits, inventories, trade and other payables and the effects of foreign exchange rates on these items.

The terms described above do not have a standardized meaning prescribed by IFRS, and therefore the Company’s definitions are unlikely to be comparable to similar measures presented by other companies. The Company’s management believes that their presentation provides useful information to investors because cash flows generated from operations before changes in working capital excludes the movement in working capital items. This, in management’s view, provides useful information of the Company’s cash flows from operations and are considered to be meaningful in evaluating the Company’s past financial performance or its future prospects. The most comparable IFRS measure is cash flows from operating activities.

About Sierra Metals

Sierra Metals is a diversified Canadian mining company with green metal exposure including copper, zinc and lead production with precious metals byproduct credits, focused on the production and development of its Yauricocha Mine in Peru and its Bolivar Mine in Mexico. The Company is focused on the safety and productivity of its producing mines. The Company also has large land packages with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

For further information regarding Sierra Metals, please visit www.sierrametals.com.

Continue to Follow, Like and Watch our progress:

Web: www.sierrametals.com | Twitter: sierrametals | Facebook: SierraMetalsInc | LinkedIn: Sierra Metals Inc | Instagram: sierrametals

Forward-Looking Statements

This press release contains forward-looking information within the meaning of Canadian securities legislation. Forward-looking information relates to future events or the anticipated performance of Sierra and reflect management’s expectations or beliefs regarding such future events and anticipated performance based on an assumed set of economic conditions and courses of action, including the accuracy of the Company’s current mineral resource estimates; that the Company’s activities will be conducted in accordance with the Company’s public statements and stated goals; that there will be no material adverse change affecting the Company, its properties or its production estimates (which assume accuracy of projected ore grade, mining rates, recovery timing, and recovery rate estimates and may be impacted by unscheduled maintenance, labour and contractor availability and other operating or geo-political uncertainties on the Company’s production, workforce, business, operations and financial condition); the expected trends in mineral prices, inflation and currency exchange rates; that all required approvals will be obtained for the Company’s business and operations on acceptable terms; that there will be no significant disruptions affecting the Company’s operations. In certain cases, statements that contain forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur” or “be achieved” or the negative of these words or comparable terminology. Forward-looking statements include those relating to the Company’s guidance on the timing and amount of future production and its expectations regarding the results of operations; expected costs; permitting requirements and timelines; anticipated market prices of metals; the Company’s ability to comply with contractual and permitting or other regulatory requirements; formalizing the refinancing contract and the timeline related thereto and the timing of senior management’s conference call to discuss the Company’s financial and operating results for the year ended December 31, 2022. By its very nature forward-looking information involves known and unknown risks, uncertainties and other factors that may cause actual performance of Sierra to be materially different from any anticipated performance expressed or implied by such forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks of not meeting the expectations contemplated herein and the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 28, 2023 for its fiscal year ended December 31, 2022 and other risks identified in the Company’s filings with Canadian securities regulators, which filings are available at www.sedar.com.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations, and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Investor Relations

Sierra Metals Inc.

Tel: +1 (416) 366-7777

Email: info@christiana-papadopoulossierrametals-com

Source: Sierra Metals Inc.