![]()

Great Bear Doubles Vertical Extent of LP Fault, Intersects High-Grade Gold at

942.20 m Downhole: 15.57 g/t Gold Over 3.05 m

March 29, 2021 – Vancouver, British Columbia,

Canada – Great Bear Resources Ltd. (the “Company” or “Great Bear”, TSX-V: GBR; OTCQX: GTBAF) today reported results from its ongoing fully funded $45 million 2021 exploration program at its 100% owned flagship Dixie Project in the Red Lake district of Ontario.

Expansion of the LP

Fault

- Deep drilling has doubled the

drill-confirmed vertical extent of the LP Fault gold zone, which begins at bedrock surface, to approximately 800 vertical metres. The area of ongoing grid drilling extends along 4 kilometres of strike length. Figure 1 and Figure 2. - Three new 400 – 450 metre step-down holes drilled along 500

metres of strike length all successfully intersected the continuation

of the LP Fault host rocks and gold mineralization at depths of 700 – 820

vertical metres. - Gold grades and mineralized

zone thickness were better at depth on two of three tested drill sections. - Initial deep drilling tested below the most weakly

mineralized segment of the LP Fault, formerly referred to as the “Gap” zone (February 13, 2020). - Large scale step-out drilling at depth,

including below areas

of high-grade gold mineralization, will continue throughout 2021.

High-Grade Gold in the First Deep LP Fault

Drill Holes

- High-grade gold was intersected at depth in two of the three deep drill holes, with better grades and thickness than previously observed in the near surface. All three deep drill holes contained multiple intervals of gold mineralization. Table 1 and Table 2.

- BR-260 is the deepest LP Fault drill hole to date. It assayed 15.57

g/t gold over 3.05 metres from 942.20 to 945.25 metres, within a broader interval of 1.08

g/t gold over 70.25 metres from 906.15 to 976.40 metres. Figure

3 and Figure

4. - While high-grade intervals are the primary drill targets at these depths, the dual high-grade and bulk-tonnage character of the

LP Fault gold zone remains strongly developed at depth. - Oriented core data collected from these initial deep holes will assist with determining controls to higher grade panels within the broad envelope of gold mineralization.

Great Bear has now published results from 270 LP Fault drill holes and anticipates at least

130 additional LP Fault drill holes will be completed by the end of 2021, for a total of at

least 400 drill holes.

Chris Taylor, President and CEO of Great Bear said, “We drilled below the most weakly mineralized segment of the LP Fault with our first deep holes, and discovered better gold mineralization at depth. After 270 drill holes we have yet to find the limits of the LP Fault’s gold mineralization. Mesothermal gold systems of this type, particularly in the Red Lake area, can extend vertically over kilometres. We are currently working with in-house and external modelers to finalize 2021 drill plans, and will provide guidance over the coming weeks on expected timing of delivery of initial estimates of mineral resources.”

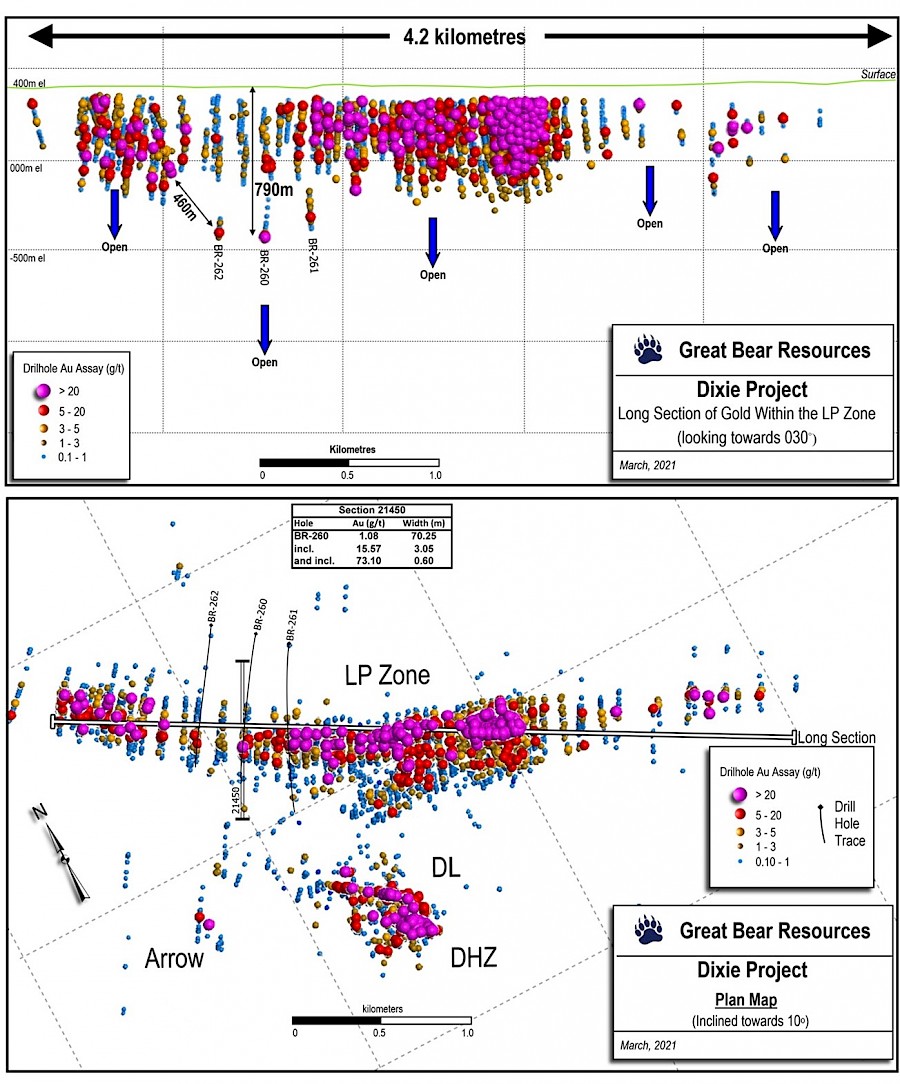

Figure 1 (Top): Long section of the LP Fault zone showing the locations and depths of the new deep drill holes (labeled).

Figure 2 (Bottom) : Map of current drill results showing the location of the new deep drill holes.

Table 1: Drill holes released to date on section 21450 showing increased gold mineralization grades and widths with increasing depth in the former “Gap” zone. See news releases of April 9, 2020 and May 4, 2020 for previously reported drill holes.

New results

from BR-260 in italics.

|

Drill Hole |

|

From (m) |

To (m) |

Width* (m) |

Gold (g/t) |

Vertical Depth (m) |

|

BR-078 |

|

176.00 |

212.90 |

36.90 |

0.42 |

150 |

|

BR-097 |

|

255.00 |

259.00 |

4.00 |

1.39 |

220 |

|

|

and |

391.70 |

393.50 |

1.80 |

3.49 |

335 |

|

BR-098 |

|

419.70 |

448.50 |

28.80 |

0.65 |

365 |

|

|

and |

493.25 |

495.05 |

1.80 |

9.90 |

425 |

|

BR-260 |

|

906.15 |

976.40 |

70.25 |

1.08 |

760 |

|

(new) |

including |

942.20 |

945.25 |

3.05 |

15.57 |

790 |

* Widths are drill indicated core length, as insufficient drilling has been undertaken to determine true widths at this time. Average grades are calculated with un-capped gold assays, as insufficient drilling has been completed to determine capping levels for higher grade gold intercepts. Interval widths are calculated using a 0.10 g/t gold cut-off grade with up to 3 m of internal dilution of zero grade.

Table 2: New drill results from the first three deep holes into the LP Fault system along 500 metres of strike length in the “Gap” area.

|

Drill Hole |

|

From (m) |

To (m) |

Width* (m) |

Gold (g/t) |

Section |

|

BR-260 |

|

906.15 |

976.40 |

70.25 |

1.08 |

21450 |

|

|

including |

929.30 |

948.00 |

18.70 |

3.33 |

|

|

|

and including |

929.30 |

929.80 |

0.50 |

16.50 |

|

|

|

and including |

942.20 |

945.25 |

3.05 |

15.57 |

|

|

|

and including |

942.20 |

942.80 |

0.60 |

73.10 |

|

|

BR-261 |

|

624.85 |

638.50 |

13.65 |

0.57 |

21200 |

|

|

|

747.15 |

761.00 |

13.85 |

0.44 |

|

|

|

|

811.60 |

823.25 |

11.65 |

0.96 |

|

|

|

including |

822.00 |

823.25 |

1.25 |

5.62 |

|

|

|

and |

835.00 |

839.50 |

4.50 |

1.17 |

|

|

BR-262 |

|

871.00 |

876.50 |

5.50 |

1.19 |

21700 |

|

|

and |

933.50 |

950.50 |

17.00 |

1.04 |

|

|

|

including |

946.50 |

948.50 |

2.00 |

7.27 |

|

|

|

and including |

946.50 |

947.50 |

1.00 |

12.30 |

|

* Widths are drill indicated core length, as insufficient drilling has been undertaken to determine true widths at this time. Average grades are calculated with un-capped gold assays, as insufficient drilling has been completed to determine capping levels for higher grade gold intercepts. Interval widths are calculated using a 0.10 g/t gold cut-off grade with up to 3 m of internal dilution of zero grade.

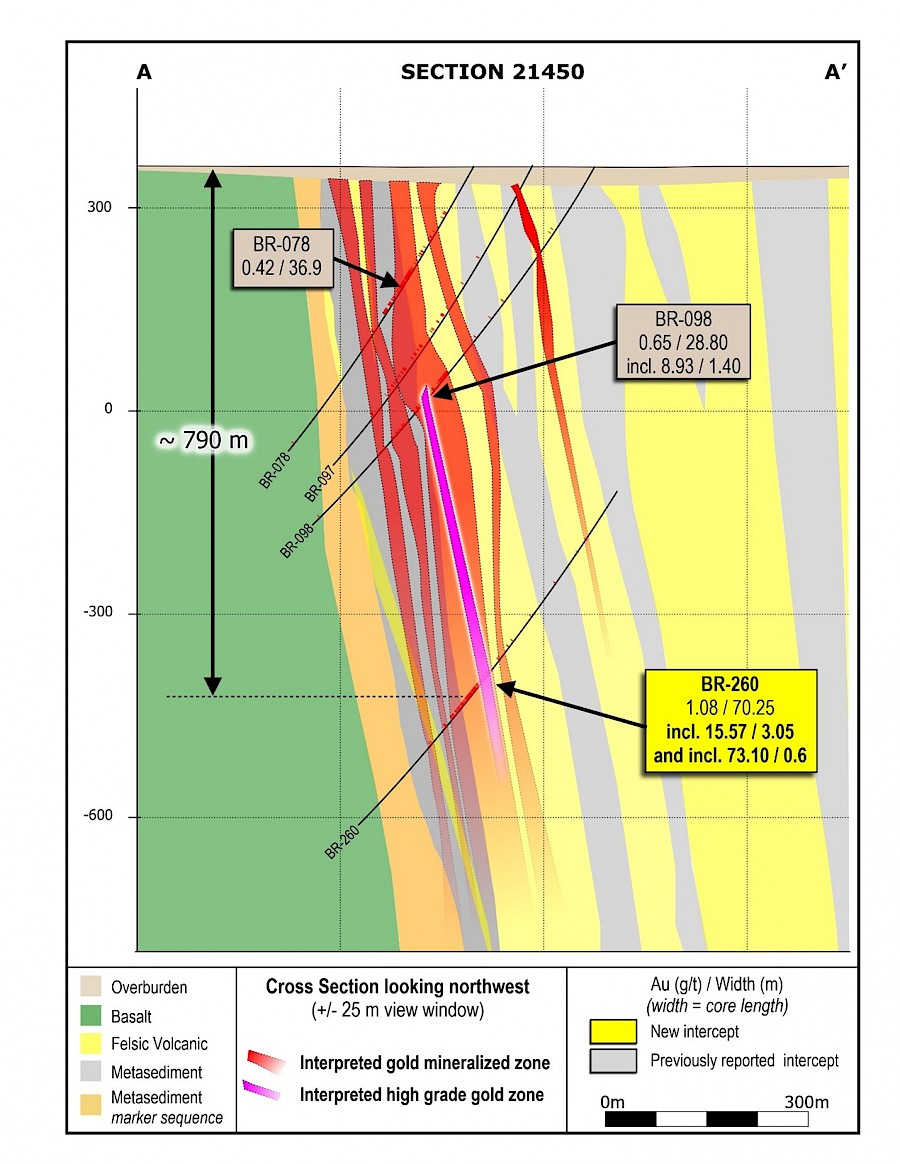

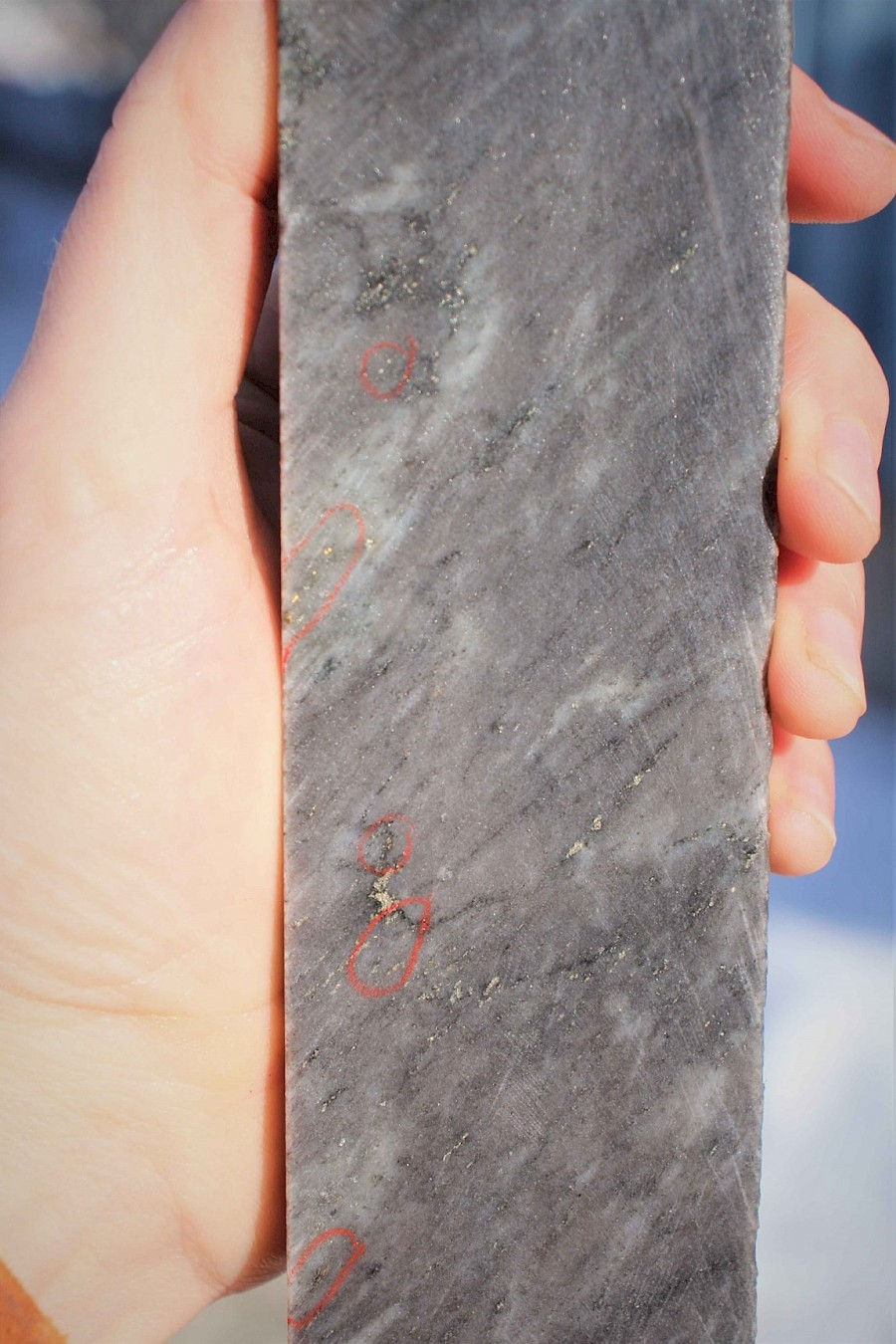

Figure 3: Section 21450 showing BR-260, the deepest drill hole in the LP Fault to date. This section is located in what was formerly referred to as the “Gap” zone.

Figure 4: The deepest drill hole in the LP Fault to date. 73.10 g/t gold over 0.60 metres at 942.20 metres down hole in BR-260 (790 metres vertical depth). The shear-zone hosted disseminated high-grade gold with sparse accessory sulphides within a felsic volcanic host matches mineralization at shallower depths within the LP Fault. Image is of a selected interval and is not representative of all gold mineralization on the property.

Great Bear’s progress can be followed using the Company’s plan maps, long sections and cross sections, and through the VRIFY model posted at the Company’s web site at www.greatbearresources.ca, which will next be updated in Q2 2021. All LP Fault drill hole highlighted assays, plus drill collar locations and orientations can also be downloaded at the Company’s web site.

Drill collar location, azimuth and dip for drill holes included in this release are provided in the table below (UTM zone 15N, NAD 83):

|

Hole |

Easting |

Northing |

Elevation |

Length |

Dip |

Azimuth |

|

BR-260 |

456566 |

5635016 |

372 |

1200 |

-64 |

225 |

|

BR-261 |

456714 |

5634887 |

364 |

1284 |

-63 |

220 |

|

BR-262 |

456384 |

5635181 |

378 |

1110 |

-63 |

224 |

About the Dixie Project

The Dixie Project is 100% owned, comprised of 9,140 hectares of contiguous claims that extend over 22 kilometres, and is located approximately 25 kilometres southeast of the town of Red Lake, Ontario. The project is accessible year-round via a 15 minute drive on a paved highway which runs the length of the northern claim boundary and a network of well-maintained logging roads.

The Dixie Project hosts two principal styles of gold mineralization:

- High-grade gold in quartz veins

and silica-sulphide replacement zones (Dixie Limb, Hinge and Arrow zones). Hosted by mafic volcanic rocks and localized near regional-scale D2 fold axes. These mineralization styles are also typical of the significant mined deposits of the Red Lake district.

- High-grade disseminated gold

with broad moderate to lower grade envelopes (LP Fault). The LP Fault is a significant gold-hosting structure which has been seismically imaged to extend to 14 kilometres depth (Zeng and Calvert, 2006), and has been interpreted by Great Bear to have up to 18 kilometres of strike length on the Dixie property. High-grade gold mineralization is controlled by structural and geological contacts, and moderate to lower-grade disseminated gold surrounds and flanks the high-grade intervals. The dominant gold-hosting stratigraphy consists of felsic sediments and volcanic units.

About Great Bear

Great Bear Resources Ltd.

is a well-financed gold exploration company managed by a team with a track record of success in mineral exploration. Great Bear is focused in the prolific Red Lake gold district in northwest Ontario, where the company controls over 330 km2 of highly prospective tenure across 5 projects: the flagship Dixie Project (100% owned), the Pakwash Property (earning a 100% interest), the Dedee Property (earning a 100% interest), the Sobel Property (earning a 100% interest), and the Red Lake North Property (earning a 100% interest) all of which are accessible year-round through existing roads.

QA/QC and Core Sampling

Protocols

Drill core is logged and sampled in a secure core storage facility located in Red Lake Ontario. Core samples from the program are cut in half, using a diamond cutting saw, and are sent to Activation Laboratories in Ontario, an accredited mineral analysis laboratory, for analysis. All samples are analysed for gold using standard Fire Assay-AA techniques. Samples returning over 10.0 g/t gold are analysed utilizing standard Fire Assay-Gravimetric methods. Pulps from approximately 5% of the gold mineralized samples are submitted for check analysis to a second lab. Selected samples are also chosen for duplicate assay from the coarse reject of the original sample. Selected samples with visible gold are also analyzed with a standard 1 kg metallic screen fire assay. Certified gold reference standards, blanks and field duplicates are routinely inserted into the sample stream, as part of Great Bear’s quality control/quality assurance program (QAQC). No QAQC issues were noted with the results reported herein.

Qualified Person and NI

43-101 Disclosure

Mr. R. Bob Singh, P.Geo, VP Exploration, and Ms. Andrea Diakow P.Geo, Exploration Manager for Great Bear are the Qualified Persons as defined by National Instrument 43-101 responsible for the accuracy of technical information contained in this news release.

ON BEHALF OF THE BOARD

“Chris Taylor”

Chris Taylor, President and CEO

Investor Inquiries:

Mr. Knox Henderson

Tel: 604-646-8354

Direct: 604-551-2360

info@greatbearresources.ca

www.greatbearresources.ca

Cautionary note regarding forward-looking statements

This release contains certain “forward looking statements” and

certain “forward-looking information” as defined under applicable Canadian and

U.S. securities laws. Forward-looking statements and information can generally

be identified by the use of forward-looking terminology such as “may”, “will”,

“should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”,

“plans” or similar terminology. The forward-looking information contained

herein is provided for the purpose of assisting readers in understanding

management’s current expectations and plans relating to the future. Readers are

cautioned that such information may not be appropriate for other purposes.

Forward-looking statements and information include, but are not

limited to, statements in respect of the proposed Offering including the

proposed use of proceeds, the closing date of the Offering, receipt of

regulatory and stock exchange approvals, the timing of future drilling,

exploration and budgets.

Forward-looking information are based on management of the

parties’ reasonable assumptions, estimates, expectations, analyses and

opinions, which are based on such management’s experience and perception of trends,

current conditions and expected developments, and other factors that management

believes are relevant and reasonable in the circumstances, but which may prove

to be incorrect.

Such factors, among other things, include: impacts arising from

the global disruption caused by the Covid-19 coronavirus outbreak, business

integration risks; fluctuations in general macroeconomic conditions;

fluctuations in securities markets; fluctuations in spot and forward prices of

gold or certain other commodities; change in national and local government,

legislation, taxation, controls, regulations and political or economic

developments; risks and hazards associated with the business of mineral

exploration, development and mining (including environmental hazards, industrial

accidents, unusual or unexpected formations pressures, cave-ins and flooding);

discrepancies between actual and estimated metallurgical recoveries; inability

to obtain adequate insurance to cover risks and hazards; the presence of laws

and regulations that may impose restrictions on mining; employee relations;

relationships with and claims by local communities and indigenous populations;

availability of increasing costs associated with mining inputs and labour; the

speculative nature of mineral exploration and development (including the risks

of obtaining necessary licenses, permits and approvals from government

authorities); and title to properties.

Great Bear undertakes

no obligation to update forward-looking information except as required by

applicable law. Such forward-looking information represents management’s best

judgment based on information currently available. No forward-looking statement

can be guaranteed and actual future results may vary materially. Accordingly,

readers are advised not to place undue reliance on forward-looking statements

or information